memo

March 14, 2022

Our first “market memo” will focus on one of Southeast Asia's largest consumer spending categories: the grocery sector. At the outset, we have a few high-level questions that we are looking to answer:

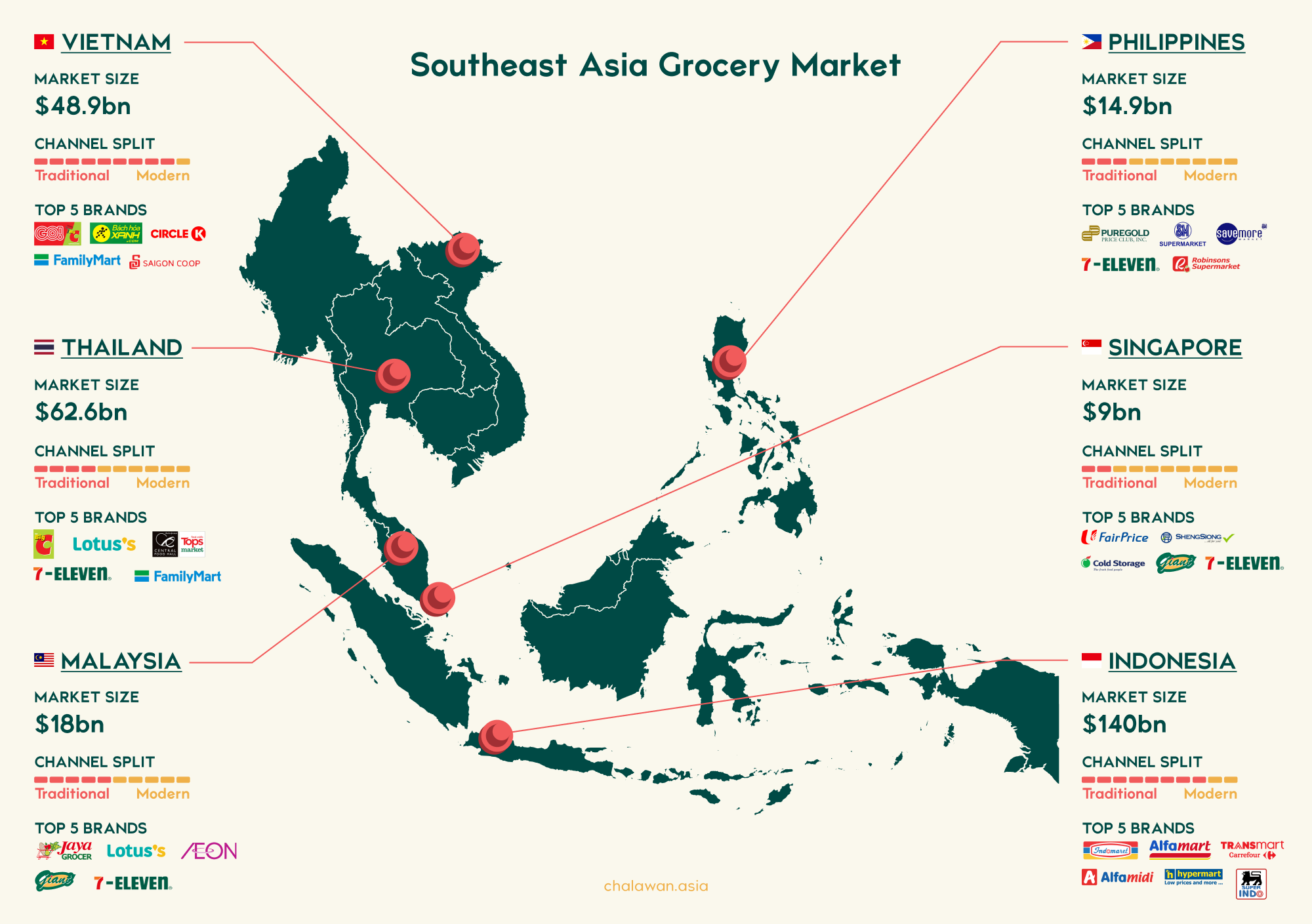

The total grocery market of Southeast Asia is estimated to reach $474.9bn by 2023, roughly the same size as Japan's. That's probably the only thing that's comparable across, with most countries in SEA looking at >7% annual growth rates vs. Japan's ~1%. The majority of sales in SEA is coming from traditional retail channels, with Indonesia and Vietnam especially dominant with >80%.

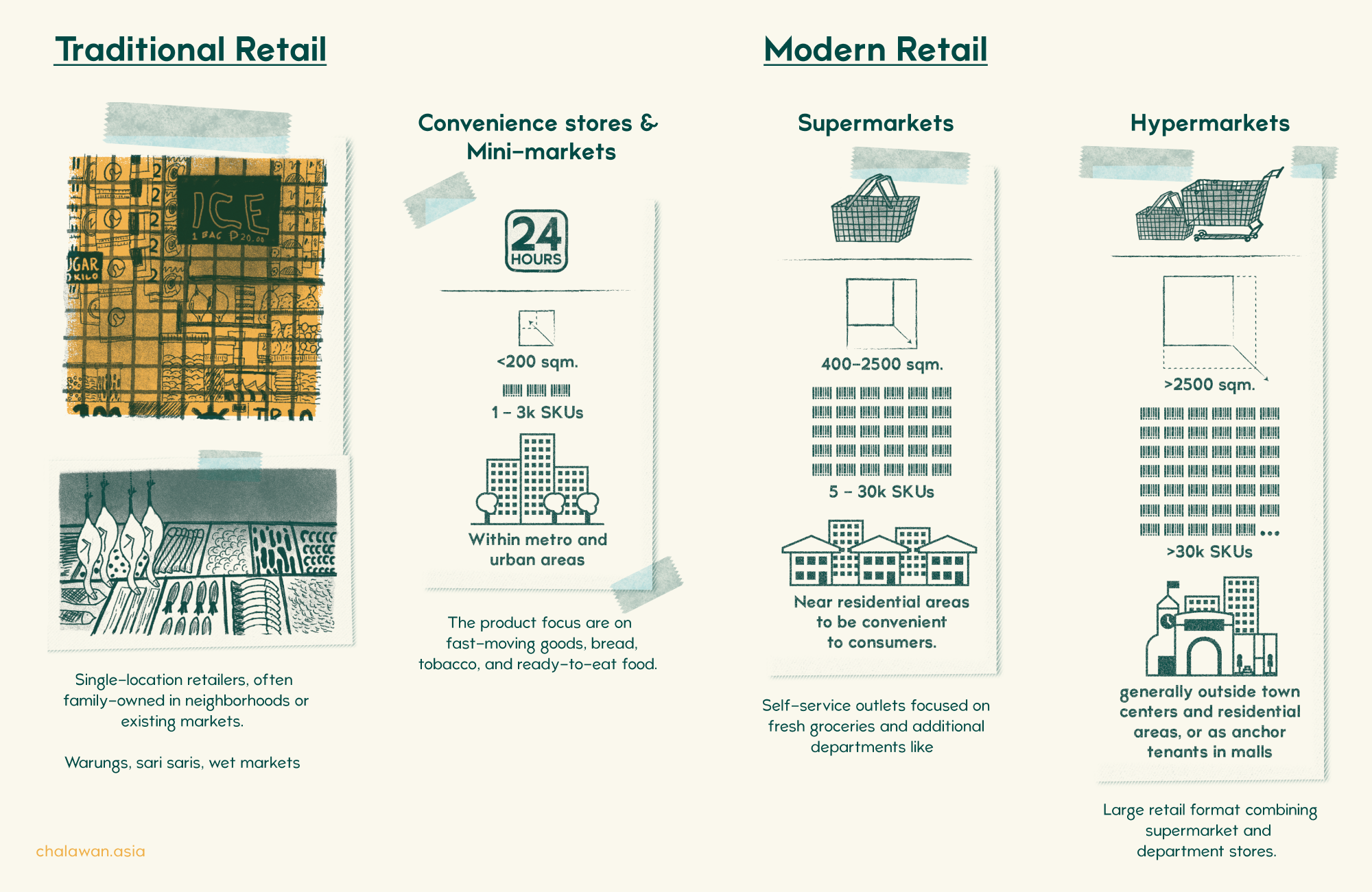

Most industry experts and reports split the grocery market into two channels:

As you can probably imagine, it's impossible to accurately categorize every single type of store there is in each market. We have been seeing an increased blurring of the lines between various retail formats, with convenience stores moving upmarket (larger product selection and bets on ready-to-eat segments) and supermarkets moving downmarket (smaller neighborhood outlets).

Nowhere is this downsizing trend more evident than in Indonesia, where Giant announced that they would be closing all their hypermarket outlets. At the same time, convenience stores Indomaret and Alfamart opened >1,000 new outlets each.

Giant is a grocery brand under the Dairy Farm International (DFI) retail umbrella, owned by Hong Kong-based trading house Jardine Matheson. DFI also operates a series of well-known retail brands across Southeast Asia, such as Cold Storage, Guardian, 7-Eleven in Singapore, and IKEA in Indonesia.

DFI announced last year that they would be completely retiring the Giant brand throughout Indonesia and shifting their focus to IKEA, Guardian, and Hero supermarkets. They see higher growth in these sectors and will be converting 5 of the large Giant hypermarkets into IKEA outlets. This echoes the changing consumer trends with valuing nearby convenience higher, and the general declining popularity of hypermarkets globally.

Giant also closed down their 3 largest hypermarket outlets in Singapore, leaving 62 smaller neighborhood supermarket outlets. The total number of stores in Malaysia has dwindled from 122 in 2018 to only 57 now. They've publicly stated that they won't open any new hypermarkets in Malaysia, focusing on growing the Giant business through the mini-market brand, Giant Mini.

One of the first things you notice when looking into the grocery market in Southeast Asia is how it's almost entirely dominated by large conglomerates, with very few independent players outside specialty outlets.

This is not unique to the grocery sector in this part of the world but more a factor of the outsized role conglomerates generally play in the economy here. I suspect we will see this exact pattern emerge in every market memo we do, which might lead us to spend more time understanding some of the most significant conglomerates impacting the Consumer space.

If you tried to draw a diagram of the top conglomerate ownership stakes in major grocery brands, you'd end up with an unwieldy criss-cross of lines (trust me, I tried). At a high level, there are some obvious characteristics in the synergies between existing conglomerate business lines and their grocery channels: (1) downstream integration with their existing supply chain, (2) sizeable real-estate portfolio.

The Thai market is mainly dominated by conglomerates, with the 3 largest ones effectively controlling the organized grocery market:

As we began our research, we realized that both of us find a bit too much enjoyment in jumping down the rabbit hole and continuously pulling at threads. To counteract this tendency and embrace a bit of "building in public," we will share any unanswered questions here. This will be a recurring section for all our market memos.

We'd also love it if these questions spark anything in your (dear reader) mind. So think of these as questions that linger in the back of our heads, and if we feel that we uncover answers through our work, we will publish them.