social commerce

June 21, 2022

This blog post is the second in our SEA Social Commerce series. Please see the announcement of our research initiative here, and the full list of social commerce archetypes here.

In this blog post we seek to shed light on the emerging social commerce archetype of live selling, and to help brands and retailers decide whether to invest in live selling in Southeast Asia.

Much has been written about this topic already, including good resources like this report from MomentumWorks and The Ken’s piece on Zalora’s Z-Live initiative. We hope to take the discussion one step further by sizing the opportunity, outlining go-to-market considerations for brands, and sharing indicative live selling economics for P&L modelling.

At the most basic level, live selling, also known by names like video commerce, live commerce, and livestreaming commerce, is a combination of internet entertainment and commerce where a presenter broadcasts live on video to an audience with the hope of selling them something. It is, in a broad sense, the internet’s answer to television home shopping (QVC).

Live selling has existed as a fringe e-commerce activity for over a decade, but a perfect storm of increased e-commerce penetration, more powerful smartphones, and faster mobile internet connections, has propelled the trend to new heights in the last few years.

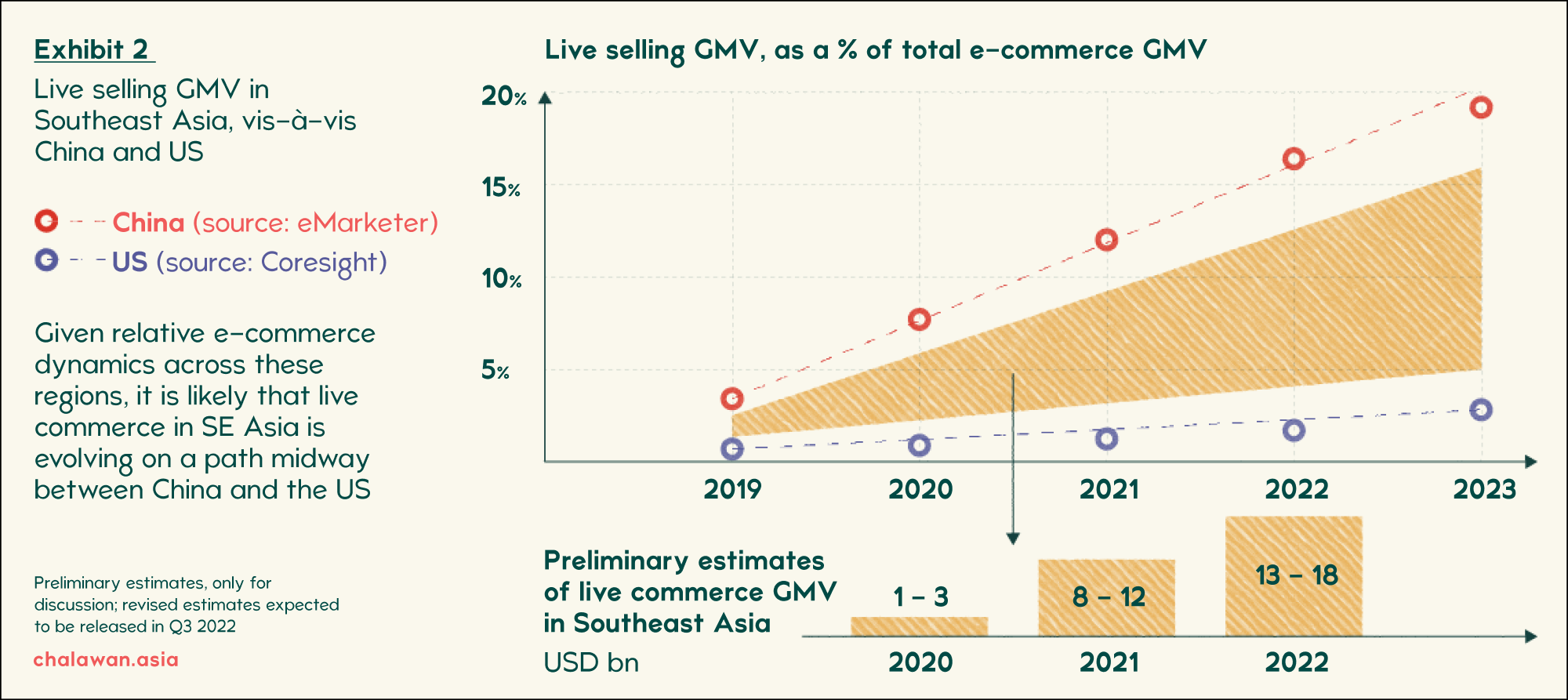

This is especially the case in China, where live selling exploded around 2019 and now drives more than 15% of all e-commerce according to eMarketer. This growth from the north has created anticipation of a similar boom in Southeast Asia. But we believe there are meaningful differences between live selling in China and in Southeast Asia.

The focus of this post is the Southeast Asian live selling market and its implications for brands and retailers in the region. We do however recommend studying the Chinese market for clues, and suggest starting with this YouTube video and this profile of Viya, one of China’s top live selling influencers.

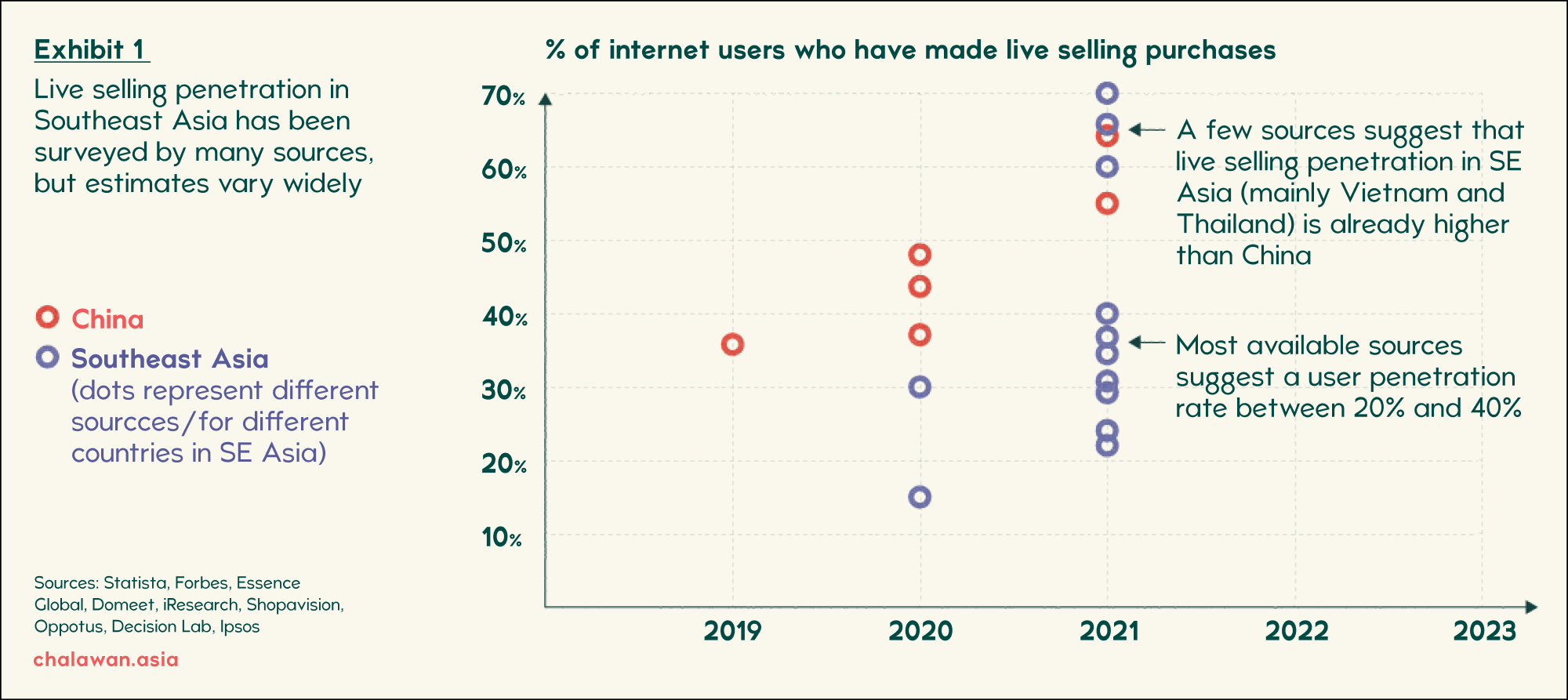

Any brand or retailer considering live selling is faced with two key questions when trying to size the opportunity: how many internet/e-commerce users buy through live selling, and what share of e-commerce GMV does it ultimately drive?

While we are conducting our own primary research to answer these questions and many more in the coming 2022 SEA Social Commerce Report, we have scoured the internet for proxy sources to present an educated guess as a start.

The first public sources started estimating Southeast Asia’s live selling penetration at the internet user level in 2020, and more joined in 2021. Estimates of 20-40% for the share of internet users who are participating in live-selling in 2022 seem to be the consensus. For comparison, in China, the world’s most advanced live selling market, equivalent estimates for this year are more than 50%.

Leveraging the insights about live selling penetration above, we can make an educated guess about live selling GMV share in Southeast Asia by comparing penetration rates with markets that are better sourced, like China and the United States. Given the total set of known dynamics, we believe this indicates a live selling market of 13-18bn USD in the region.

We will share more details on the market sizing, including estimates for each of the regional markets, in our upcoming report. For now, we believe these estimates add credibility to the hypothesis that live selling contributes to a meaningful share of e-commerce in Southeast Asia, and that it will likely continue to grow fast in the coming years. As a result, brands and retailers in the region will need to decide whether to enter, and if yes, how to do it.

Live selling in Southeast Asia is still at the early adopter stage. Consumers are constantly evolving their engagement behaviour, and live sellers and platforms are doing their best to keep up. The result is a very high rate of innovation and a dynamic landscape of sellers, buyers, platforms and enablers. However, some best practices are emerging, and we believe they can be useful for anyone who is considering how to start live selling.

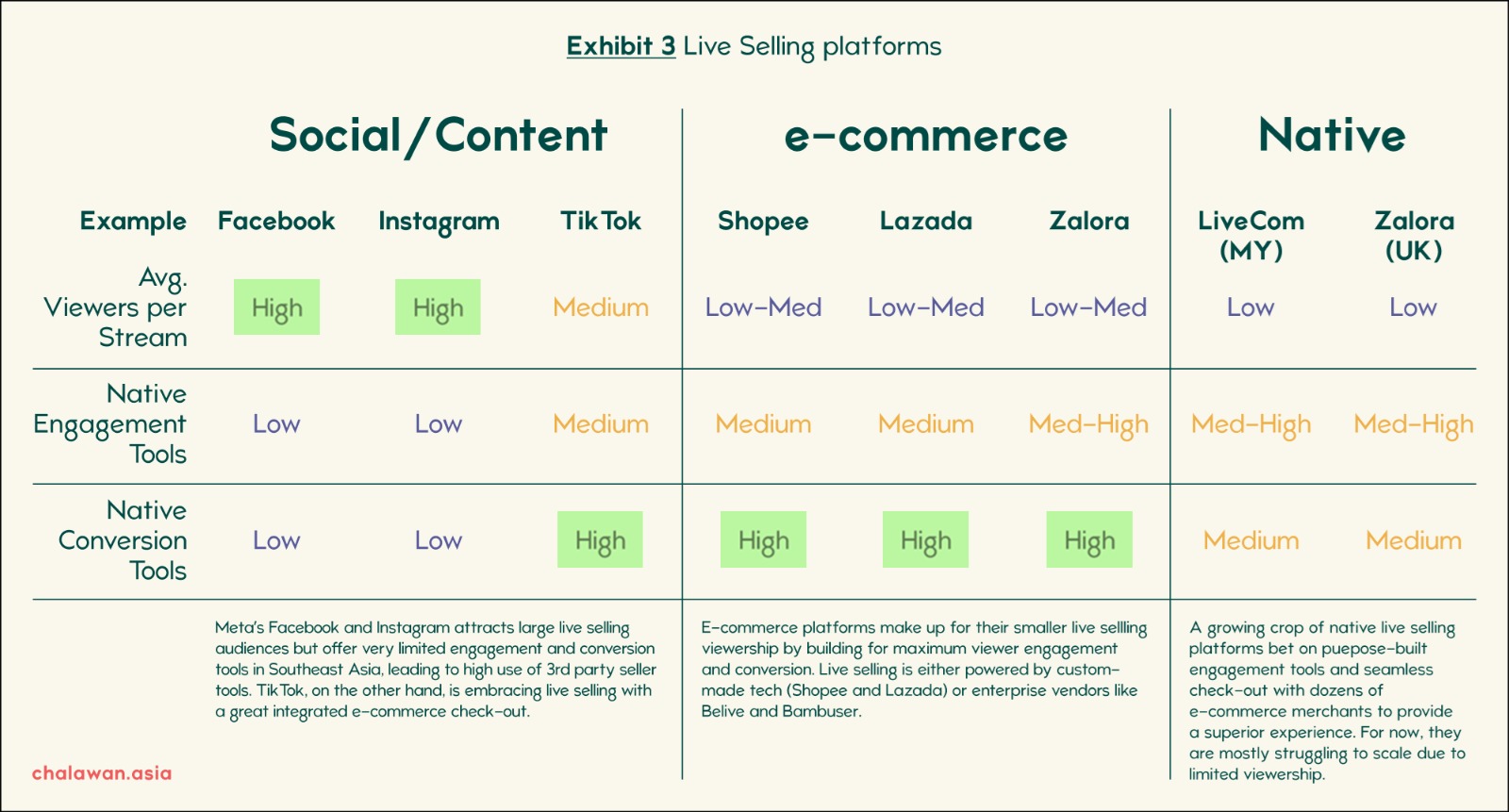

There are currently three types of platforms for live selling in the region - social and content platforms, e-commerce platforms, and a growing set of app-based native live selling platforms. While tools to simultaneously cast a feed of video to multiple platforms exist, complexities related to audience engagement and transaction capture make it challenging to execute this “multicast” live selling well. In other words, live sellers have to choose a primary platform, and each comes with its own set of trade-offs. We believe the most important traits of live selling platforms are:

The exhibit below outlines some of the pros and cons of each type of platform. Scroll past the exhibit for more detail on each platform type.

When live selling started to proliferate in Southeast Asia around 2018 and 2019, the Meta ecosystem - consisting of Facebook and to a lesser degree Instagram - was where most of the action started. Brands and influencers with an existing audience were able to find immediate viewership, and new sellers could lean on Facebook’s discovery and sharing algorithms to build an audience. The trade-off however, is that Meta has never taken significant steps to improve its live selling engagement and conversion tools. TikTok has taken a starkly different path, mirroring the integrated e-commerce tools of its Chinese sister-app Douyin to provide fully integrated online check-out, even in its early days of user growth. As a result, the two ecosystems provide different value to live sellers:

We believe social and content platforms are a good place to start for brands and retailers who want to try live selling. Facebook and Instagram work well if you have an existing platform audience and the ability to capture e-commerce orders elsewhere, but TikTok is a much more vibrant and live selling-friendly platform that is poised for growth - particularly with younger audiences.

While the emergence of live selling on social platforms was driven more by enthusiastic streamers than the spartan infrastructure, live selling through e-commerce platforms has been very deliberately instigated by the two dominating e-commerce marketplaces in Southeast Asia, Shopee and Lazada. Both learned best practices from Chinese e-commerce giants like Taobao and JD and applied them in Southeast Asia. More recently, another type of e-commerce platform live selling has emerged, with individual brands or retailers creating live selling destinations inside their website or app. Both channels offer trade-offs:

If social platforms provide the best stage for live selling audience generation, e-commerce platform live selling is tailored to help engage and convert traffic that already exists. We recommend most brands and retailers to be more careful on platforms like Shopee and Lazada due to the low viewership and brand-risky seller environment, while any brand with a large existing D2C e-commerce business (>10mn USD per year in sales) should explore independent e-commerce live selling to maximise engagement, conversion and repeat orders.

The latest addition to the live selling platform landscape is so-called native live selling platforms. These are most commonly venture-backed start-ups and dedicated fully to a mobile experience, either through an app or a mobile website. Notable examples include Livecom (Malaysia) and Ooooo (England). These platforms aim to marry a high-quality set of engagement and conversion tools with integrations to multiple e-commerce sites, allowing influencers and independent presenters to stream and sell easily, and to earn money through a revenue share agreement.

While these platforms are conceptually interesting, most are still in a very early stage of their development and do not offer compelling alternatives to the social or e-commerce platforms listed above. Many also do not have sufficient viewership or activity to warrant focus by big brands at this point.

Although live selling is still in its infancy in Southeast Asia, low barriers to entry mean that there are thousands of live selling livestreams active at any given moment. Consumers can only view one livestream at a time, so there’s sharp competition for viewership. Three categories of live selling streamers vye for those eyeballs today, each employing different techniques and tactics to engage with and convert viewers. We’ve described each live seller type in detail below:

This segment, containing micro-sellers of all kinds, is by far the largest by quantity, but at the same time also the hardest to understand. It includes anything from local clothing shop owners to toy importers, and is characterised by a couple of distinct traits:

Independent live sellers can appear like an attractive target segment for brands and retailers due to their high aggregate GMV, but lack of scale, high discounts, and branding risks mean that very few organised sellers have succeeded in generating sustained sales through this channel so far.

As live selling has become more well-known, more and more established brands are experimenting too. They tend to pick one of two common angles of attack; one group, like Uniqlo Thailand, starts by streaming to their existing Facebook audience with conversions happening on their website, while another, like Adidas Malaysia, partner with an e-commerce platform like Shopee to host live sessions in conjunction with a brand launch or major sale. A couple of dynamics are emerging among this set of established live sellers:

For established brands that consider live selling, shadowing first-mover brands and retailers is a great way to gain a basic understanding of best practices. That said, the sample size of active brands is still very small, and only a few have successfully evolved live selling from the experiment stage to real recurring operations.

Social media influencers is no new concept in Southeast Asia, where the vast majority of brands and retailers work with ‘key opinion leaders’ to generate awareness, engagement and conversion around new launches, sales and more. But live selling influencers, who have risen to fame due to their infectious personalities and selling skills, are a very different breed:

Influencers hold massive sway over what moves in live selling, making them an attractive tool for brands and retailers that want to grow live sales fast - whether through the influencers’ own channel or by hiring them as a presenter for the brand’s channel. We caution aspiring sellers to be careful in evaluating the brand-fit of each influencer, and to structure commercial terms in a way that guarantees success both at the topline and bottomline. There are many agencies and multi-channel networks that are emerging to help brands make these decisions, like Nuffnang Live (Malaysia) and Pongo (Indonesia).

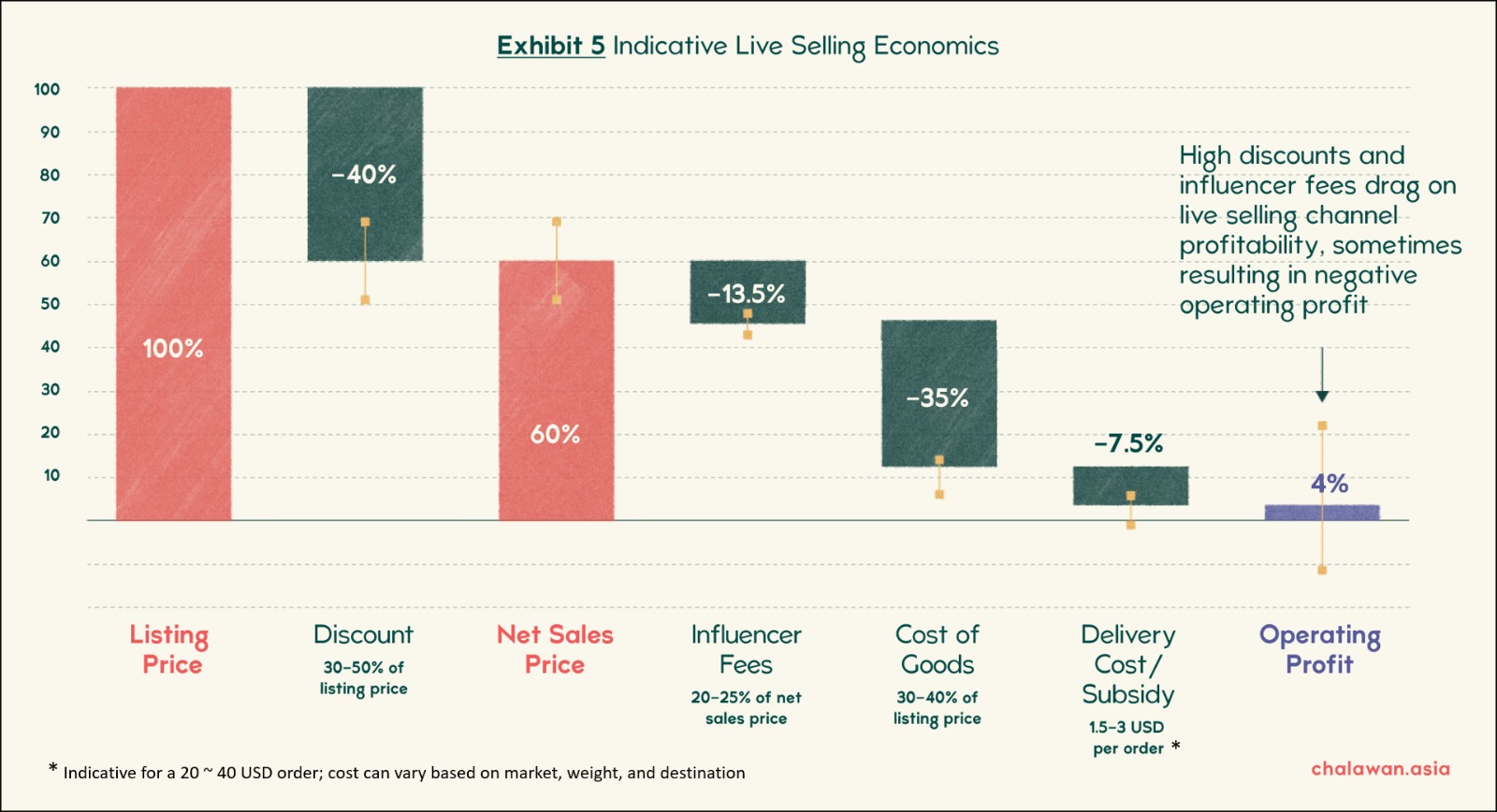

Like e-commerce in general, live selling ultimately only makes sense if it generates profit. The costs of live selling depend greatly on how it is carried out; for example, whether an e-commerce platform like Shopee takes a cut of sales, whether a famous influencer is needed to help drive traffic, and whether tech vendors and agencies are required. Two cost elements deserve extra attention in live selling P&L modelling:

We’ve shared an illustrative example of live selling unit economics below, based on a scenario where an established brand partners with a top live selling influencer to sell through a social platform, with commercial arrangements that still seek to achieve a positive bottom-line result for the brand:

As a general rule of thumb, live selling carries a similar cost structure to general e-commerce, except for a slightly higher discount provision and the fact that digital marketing spend is replaced by revenue share fees to the influencer generating sales.

Live selling is a large and fast-growing part of the Southeast Asia social commerce landscape. It was created in an unlikely crucible of Western social platforms (Facebook and Instagram), local e-commerce leaders (Shopee and Lazada), and a healthy dose of inspiration from the Chinese e-commerce market. Now, a couple of years on, those elements are coming together in a selling environment that is unique to Southeast Asia.

While independent sellers and influencers have been quick to seize the opportunity of this new market, established brands and retailers as a whole have not done much. We believe this is more due to a lack of go-to-market guides, tools and case studies than any inherent risks or disadvantages of live selling as a sales channel. Brands that aspire to lead in their e-commerce category in Southeast Asia must contend with this new space and set a strategy for live selling.

We will continue to expand our set of live selling resources for brands and retailers, including granular market sizing, go-to-market guides and case studies. Please sign up to the Chalawan Insights newsletter below to receive our coming posts, and e-mail simon@chalawan.asia for any further assistance or feedback.

This post is created in collaboration with Matias Singers and Sarabjit Singh.