social commerce

September 26, 2022

This blog post is the fourth in our SEA Social Commerce series. Please see the announcement of our research initiative here, and the full list of social commerce archetypes here.

In our previous blog posts we’ve covered two social commerce archetypes - Live shopping and Conversational commerce - that elevate traditional e-commerce by injecting distinct social traits into the customer experience. In today’s post we explore a social purchasing experience of a different type in the archetype of Community group buying, where brand-new actors like agents, resellers, community leaders and B2B distribution platforms are upending how consumer goods are bought, sold, and distributed across Southeast Asia.

This model really took off during the COVID years, especially beyond the Tier 1 cities, and has resulted in a new kind of e-commerce and a potentially significant market disruption. A whole segment of users in the region is being engaged as agents or group leaders. And venture capitalists have added fuel to the fire, funding more than two dozen new start-ups (like Super in Indonesia and Aemi in Vietnam) to fight for a spot in the Southeast Asia’s consumer goods markets of tomorrow.

In this post we seek to add to the conversation about Community group buying in Southeast Asia by proposing a definition, expanding on important dynamics like value drivers and the role of agents, and discussing the implications for brands and retailers in the region.

To understand what Community group buying is all about, it is helpful to invert and think first about a regular e-commerce or bricks and mortar purchase journey. In those instances we might act on the recommendation of a friend or family member to visit a store or purchase a product, but otherwise the transaction happens between us, a single consumer, and a professionally run store.

Where Community group buying differs is that it introduces groups - friends, family, or other members of our communities - as participants in the e-commerce value chain. This dynamic, which builds on a number of disparate factors including Southeast Asia’s unique community culture and the innovations of Chinese tech companies, has resulted in brand-new ways of buying and selling consumer products in Southeast Asia.

At a high level, we see two emerging models in Southeast Asia’s Community group buying landscape:

We’ve explained both models below.

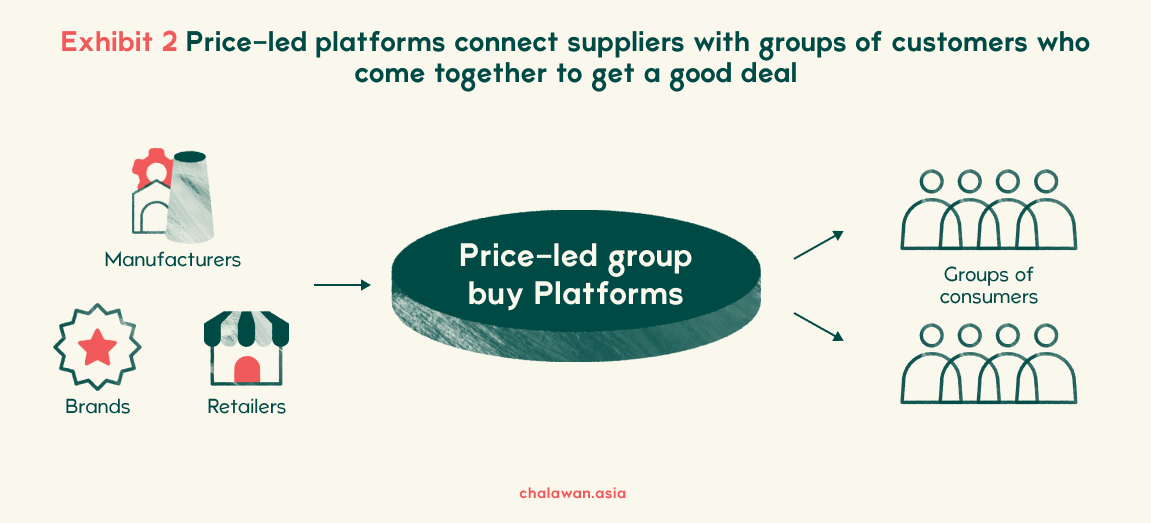

The Price-led variation of Community group buying focuses on pooling consumer demand for certain products by offering a time-limited discount or deal in return for guaranteed purchase participation.

The most famous example of Price-led Community group buying is China’s Pinduoduo, which was launched in 2015 and has since grown to annualised sales of more than US$ 15bn. Pinduoduo provides a platform that lists thousands of deals on products like fresh vegetables and home goods, and consumers are encouraged to form ‘teams’ of friends and family members who commit to buying within a 24-48 hour window in return for an attractive discount or gift with purchase. This video from KrASIA is slightly dated but provides a useful introduction to Pinduoduo’s model, which the company calls ‘team commerce’.

In the video above, the company’s CEO Colin Huang shares that “before July of 2017, we never used commercials or ads to promote ourselves.” That is possible because the primary value proposition of a Price-led model is the group discount, which sets up an organic incentive for users to share the deal with their family and friends, without necessarily needing a central coordinator or group leader to nudge them to do so.

Of course, some nudges are always helpful. Which is why, the Price-led model sometimes introduces the role of a so-called lead consumer, who takes the initiative to gather a group of friends or family members to unlock the discount. In some cases this lead consumer receives an additional discount or other benefits for their efforts, but this is not always the case and rarely ever amounts to more than a couple of percent of the sales volume generated from the group purchase.

The success of Pinduoduo in China has led several players to attempt to bring the Price-led Community group buying model to Southeast Asia. But the results so far have been underwhelming.

Lazada launched its community group buying feature Slash It in 2020 but rarely showcases it outside major campaigns, and Shopee offers a group buying feature in several markets but does not promote it actively.

Among start-ups, one of the most well-known community group buying platforms is Singapore’s WeBuy, who acquired an Indonesian peer called Chilibeli in 2022. WeBuy started with a focus on the price-led value proposition of group buying, but our own spot checks of its customer experience indicate that they seem to have changed their focus from being price-led to a broader set of social commerce features anchored around their group leaders, further indicating that the original model has not taken off in Southeast Asia.

We believe a host of factors contribute to the lack of adoption of Price-led Community group buying in Southeast Asia, despite the tremendous success that Pinduoduo saw in China. We have summarised them in the exhibit below. With the continued growth of e-commerce and its requisite infrastructure, it is possible that Price-led community group buying will pick up in some small segments in Southeast Asia in the future. We do not however see it scaling up here to anything like the size of Pinduoduo in China.

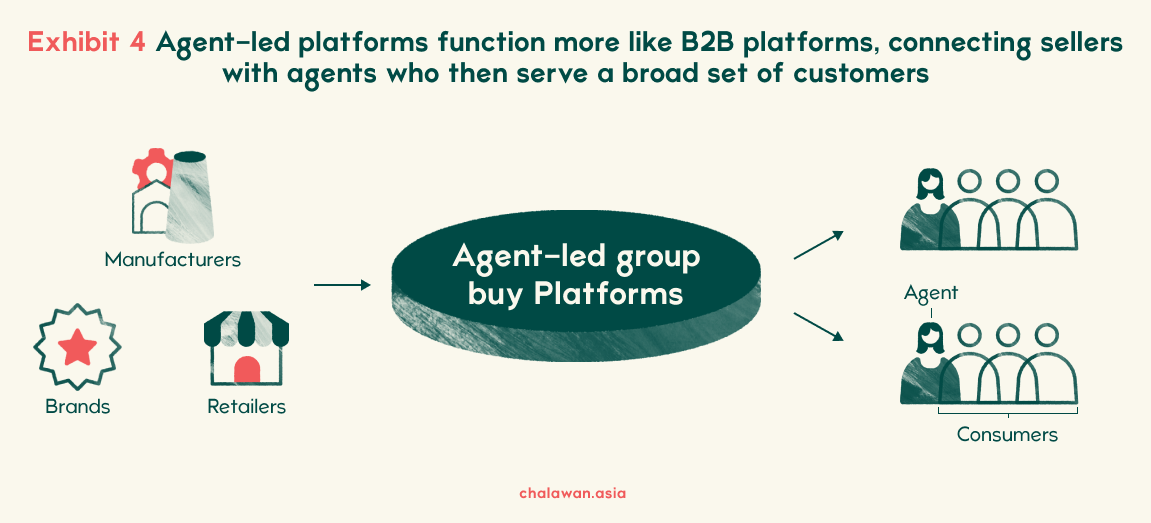

Where the Price-led Community group buying model relies on consumers to form spontaneous groups and commit to purchase in return for a great deal, the agent-led community buying model introduces two new and fascinating roles: the agent, also referred to as the reseller, and the B2B distribution platform.

In this type of Community group buying, a social microseller partners up with a B2B distribution platform to get access to products and selling tools, and serves a set of consumers - in most cases in their nearby areas - almost like a traditional retailer would. The B2B distribution company in turn manages wholesale partnerships with manufacturers and brands, who are not set up to manage hundreds or thousands of ‘mini-retailer’ agents on their own.

While the exact dynamics of this selling model differ across countries and categories, it provides similar value across the board:

We have included a more complete discussion on the roles and value drivers of market participants of community selling later in this blog post.

This model provides obvious value and synergies in a region like Southeast Asia where consumers are scattered and retail infrastructure is still sparse. Not surprisingly, this has led to an enormous influx of start-up funding in the space, resulting in dozens of new companies vying to be the favourite platform of Community group buying agents.

A handful of the many players in the Agent-led Community group buying space are:

Some may claim that many of the startups above are just B2B distribution or B2B e-commerce companies dressed up in the fancy language of “social commerce”. We’ll leave that judgement to our readers on a case by case basis for each.

Regardless of what we call them though, we believe the Agent-led Community group buying model has some scale and growth potential across Southeast Asia for several reasons. Three stand out as the most important:

In our previous posts, we have addressed the challenge of there being very limited, good-quality data available on market sizing for social commerce in Southeast Asia. For the Community group buying archetype, that challenge is multiplied a few times over - the model seems to have emerged a bit under the radar in the last few years, its success has been relatively patchy (for example, there are many more Community group buying startups in Indonesia versus Thailand), and the boundary between a B2C Community group buying platform that targets resellers (which is social commerce) and a B2B e-commerce platform (which is not) can be hard to make out.

Nevertheless, a useful data point is in Facebook’s most recent Sync Southeast Asia report just released this month, which estimates group buy to be ~ 3% of total e-commerce in the region, or around 5bn USD according to their estimates of the total e-commerce market. Other helpful data points are from China - the Chinese Community group buying market in 2021 has been sized from 120bn CNY by Statista up to 180bn CNY by Bain, both ~ 1% of the Chinese e-commerce market. Interestingly, both these estimates seem to exclude Pinduoduo, whose GMV alone is around 15-20% of total e-commerce in China.

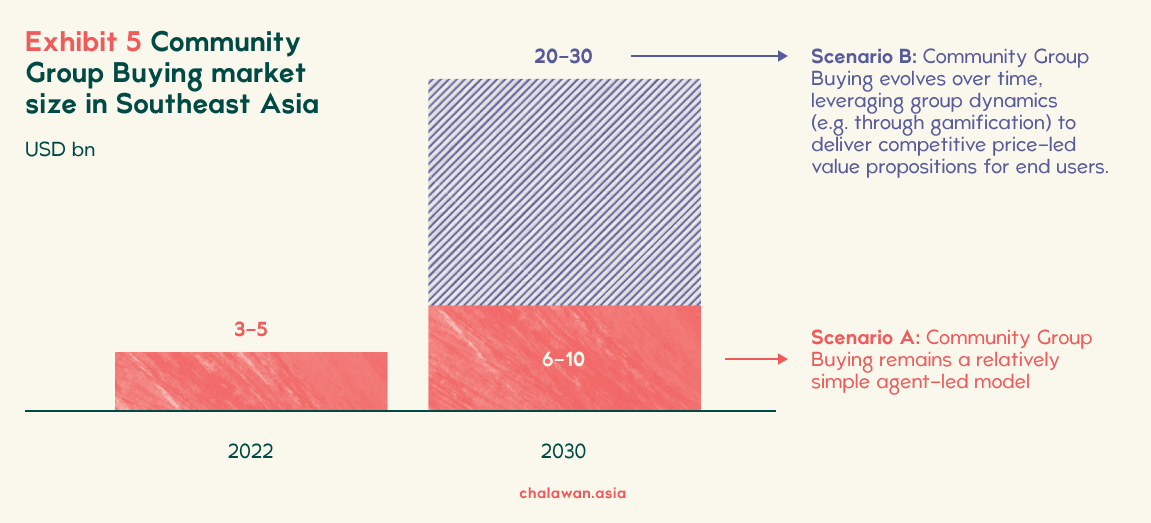

Considering the data points above, a reasonable estimate for the Community group buying market in Southeast Asia could be around 3-5bn USD in 2021.

Comparing Southeast Asia and China this way reveals an interesting dynamic - that in terms of penetration, the Community group buying market in Southeast Asia (at least the Agent-led model) could be bigger than China! There are not many businesses you can say this about. But as we have explained later in this post, the dynamics of the Community group buying model are unique, and particularly suited for developing markets with populations that have not yet fully matured in using e-commerce.

Looking forward therefore, two scenarios emerge:

In the first scenario (A), Community group buying remains dominated by relatively simple, agent-led models suited to help unsophisticated users who cannot shop online themselves. In this scenario, as e-commerce in Southeast Asia penetrates deeper beyond Tier 1 cities into Tier 2 and Tier 3, the emergence of new customers that agents or resellers can target will be counterbalanced by the “graduation” of end users who will begin to shop online themselves. In this dynamic equilibrium, Community group buying will grow in line with the total e-commerce market, and its share will remain more or less the same as today.

In the second scenario (B), Community group buying models are able to remain relevant to these “graduating” users even as they become more sophisticated, and find innovative ways - like Pinduoduo has in China - to continue to offer attractive prices through group dynamics in ways that other e-commerce platforms cannot match. If they can achieve that, users who begin their e-commerce journeys with Community group buying will be more sticky, driving up the total share of e-commerce for this model over time..

Exhibit 5 below illustrates these 2 scenarios:

Compare these forecasts with a quote from Vincent Xue (co-founder and CEO of WeBuy), who had mentioned in a 2021 interview with e27 that “we believe that the market size for community group-buy models in Southeast Asia will reach over US$10 billion within 10 years.” Vincent may not have done the scenario analysis in the same way as we have above. But his estimate underscores a key point. Between the two scenarios painted above, achieving Scenario B will be more challenging, as group dynamics, in of themselves, do not translate to cost advantages in Southeast Asia as readily as they do in China (a few reasons outlined in Exhibit 3 above).

The rest of this post goes into the dynamics of Community group buying, how the model sits alongside other forms of retail, and what these competitive differentiators mean for its future.

While the economic viability of social commerce archetypes like Live shopping and Conversational commerce can be explained neatly through their measurable impact on e-commerce metrics like conversion rate and purchase frequency, grappling with the short-term and long-term impacts of Community group buying is harder because it tends to not just augment existing distribution channels, but also replace them in some cases.

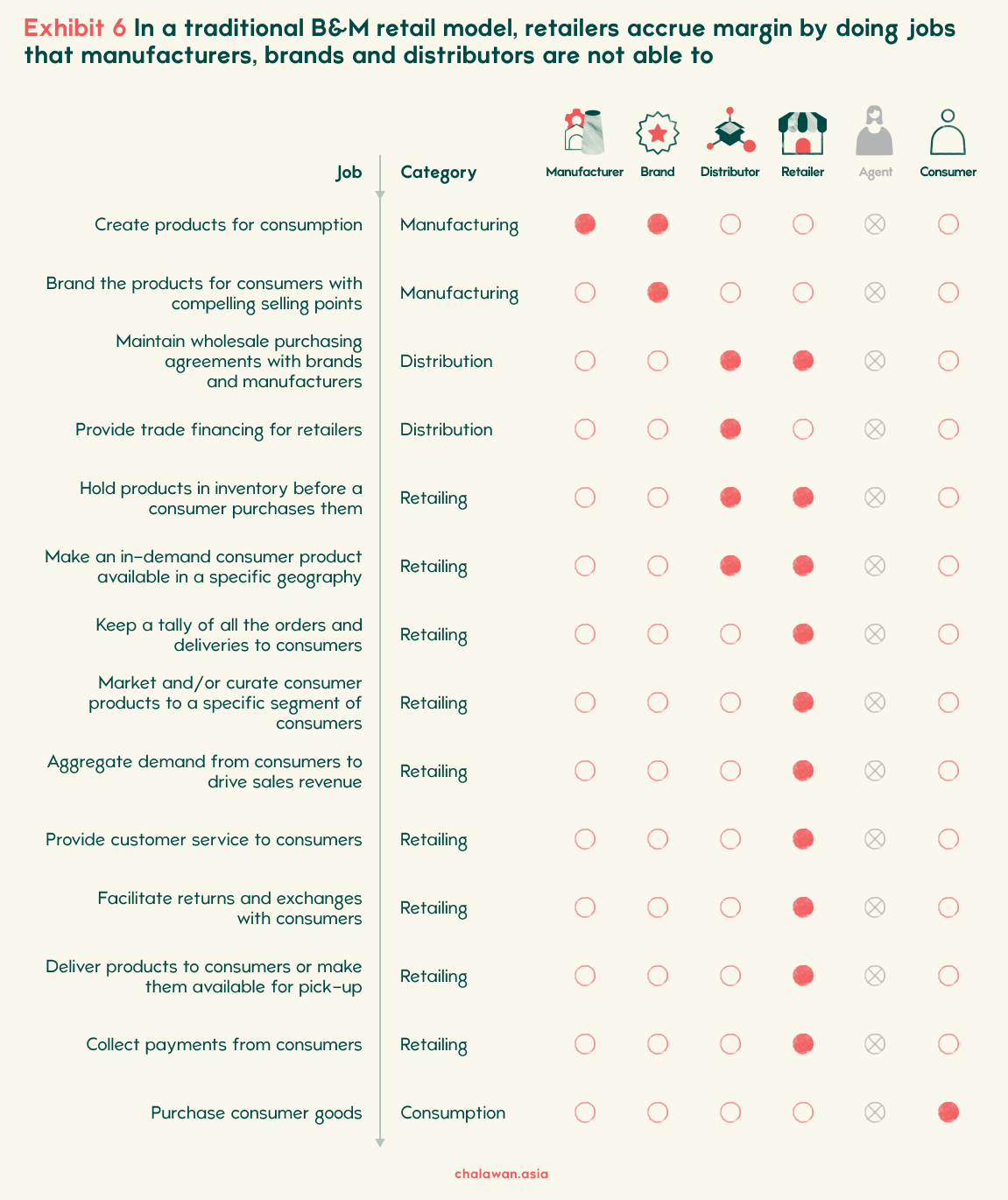

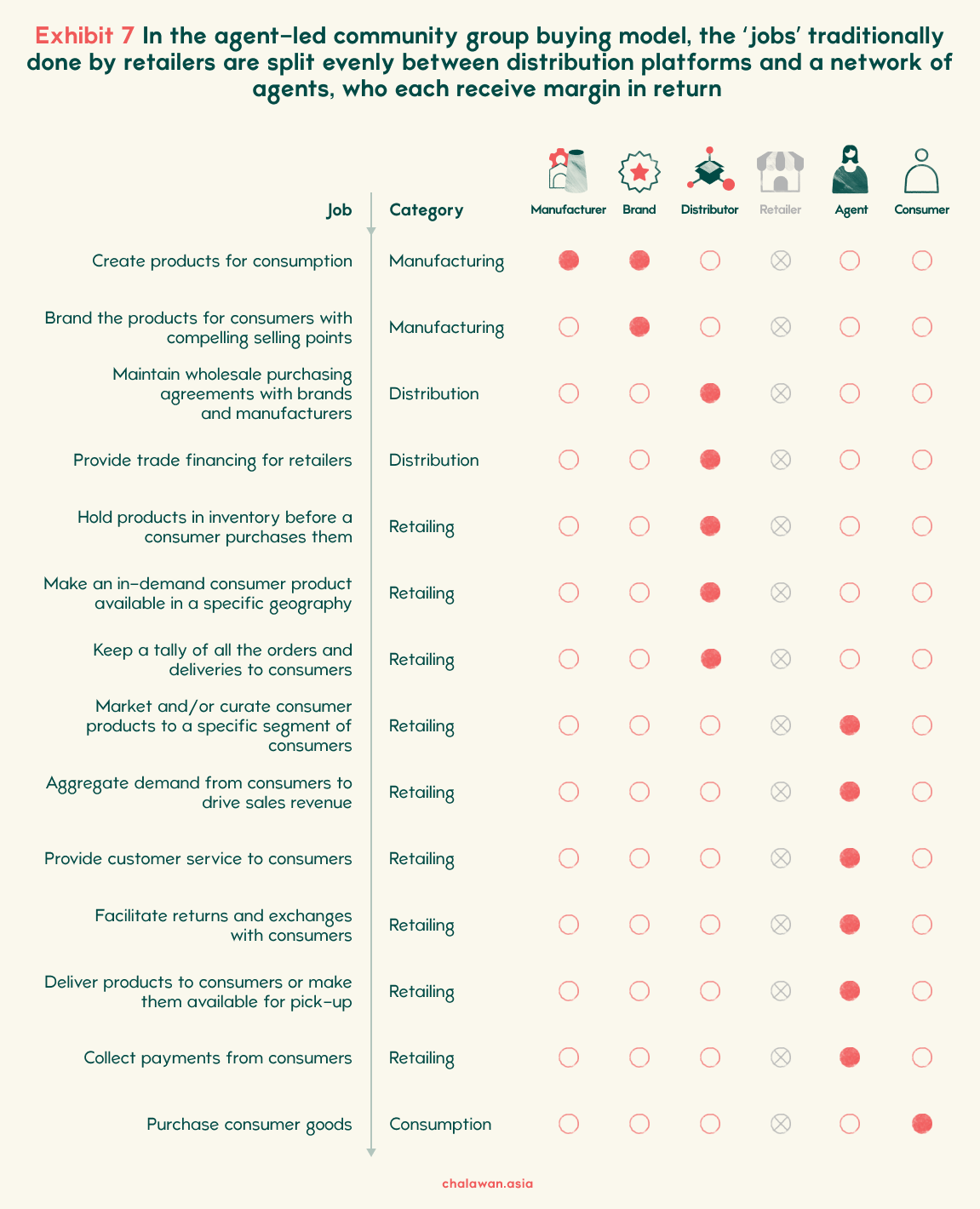

To better understand what this new model of selling has done to Southeast Asia’s retailing landscape, and to understand who might be benefiting and hurting from its growth, we use the framework of ‘Retailing jobs to be done’ to compare it with the traditional retail model and hypothesise where margin might be distributed and accrued in each case.

The basic concept of the framework is that there is a list of at least 14 distinct jobs across 3 steps of the value chain to be done for a consumer good to reach the hands of a consumer, as shown in Exhibit 6 below. Any seller who can do all these jobs would accrue 100% of the final selling price to the consumer, but likely also incur very high costs of doing those jobs due to lack of specialisation. A more common equilibrium point will include several players working together to do the jobs, and hence the economical value of the purchase will be split between them.

To set the scene, the above exhibit outlines the distribution of jobs to be done for a sale of Adidas branded shoes through the JD Sports retailer in Singapore.

In this instance the manufacturer and brand work together to create the shoe, the distributor holds inventory and brings it closer to points of sale in bulk, and retailers do a long list of jobs including demand aggregation (through operating stores and doing marketing), customer service, making products available to consumers, etc. Finally consumers purchase the products, completing the loop.

In this traditional model the margin of the selling price will be split between the retailer, the distributor, the brand and the manufacturer.

In the Agent-led Community group buying model illustrated above, based on the Indonesian reseller platform Raena, we see how the jobs to be done shift from the more traditional model in the previous example. While platforms’ value proposition differs slightly, this breakdown is broadly applicable to players like Aemi and Selly, too.

In this model, the jobs to be done that are traditionally performed by the retailer are instead split neatly between B2B distribution platforms (like Selly and Raena) and their agents. B2B distributors deal with brands and manufacturers, hold inventory, provide trade credit and often ship products to the agents, while agents are responsible for generating demand in their local community, performing customer service, and collecting payments from customers. That in turn allows Agents (who are often relatively unsophisticated micro-sellers) to take over the remaining tasks that would have been performed by the retailer, effectively eliminating the retailer altogether.

There is no doubt that Community group buying has shaken up Southeast Asia’s consumer markets, particularly driven by the fast-growing Agent-led model. However, it is worth asking whether this development is sustainable, or whether it will subside again.

For reasons shared in section A above, the Price-led Community group buying model has failed to really take off in Southeast Asia in a big way. In fact, following the remarkable cooling of investor sentiment towards cash burning startups this year, questions about Pinduoduo’s own model in China are getting louder.

But the Agent-led Community group buying model is not facing these long-term sustainability questions, at least not so many and not just yet. That is because where the Price-led model optimises for lower prices by yielding most of the traditional retailer margin to consumers in the form of deals and discounts, the Agent-led model interestingly seeks to maintain healthy margins that accrue to the agent and distributor against a promise of better customer experience.

While this sounds great in theory, there are challenges ahead. We believe the three most important are:

We’ve explored these below.

Because the Agent-led community group buying model introduces significant transparency into retail distribution, price competition is likely to pressure distributors and agents over time. Multiple distributors will fight for the same brand and manufacturer deals, and multiple agents will fight over the same consumer and offer prices closer and closer to their wholesale purchase level.

This element of competition is likely to erode channel margins among distributors and agents specifically, but manufacturers and brands also face financial risks when entering agent-led community selling. That is because the model is much more likely than traditional retail to expose wholesale prices to consumers, either through their own online research or through conversations with individual reseller agents.

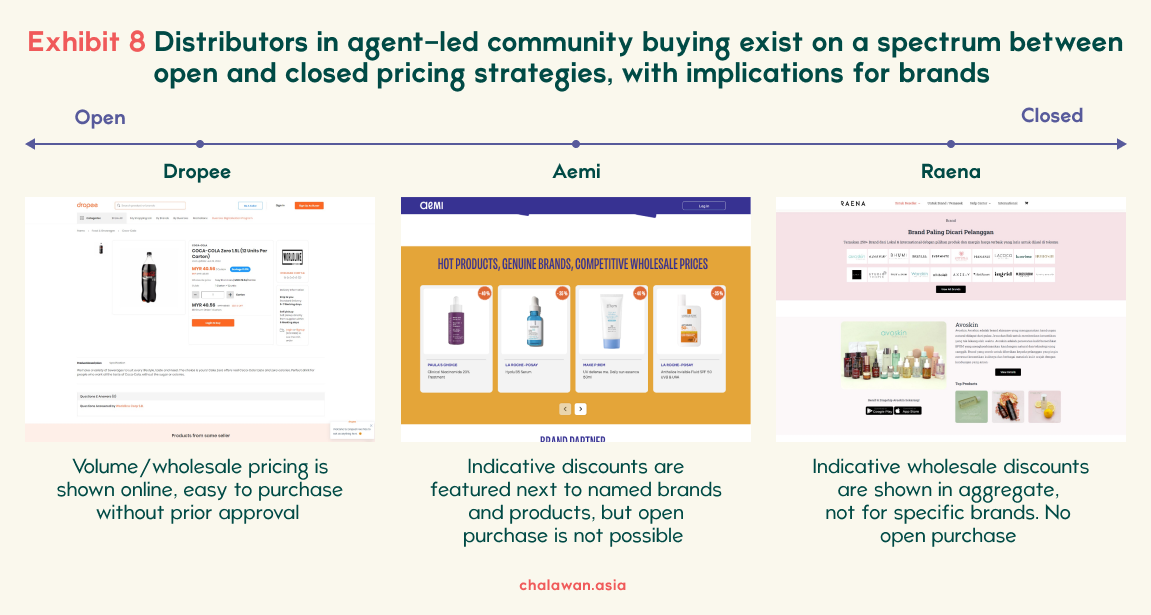

This is where it becomes important to dig deeper into this model to understand the two broad types of Agent-led Community group buying platforms based on their pricing strategies.

Nothing in this world is black and white of course. So there also exist hybrid platforms that are in between the Open-to-Closed spectrum. We’ve shown some examples of this in the below exhibit:

From a long-term sustainability perspective, we believe that B2B distribution platforms that are nearer the closed end of the price transparency spectrum are better able to help their brand partners uphold pricing power and maintain good relations with other distribution channels.

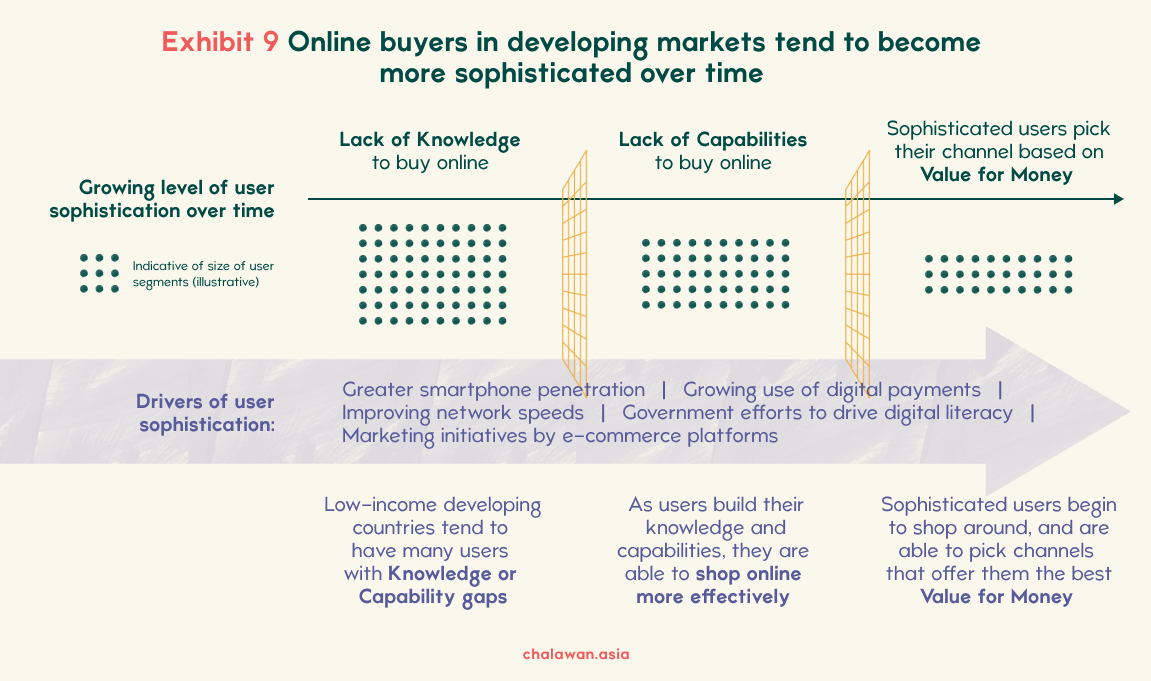

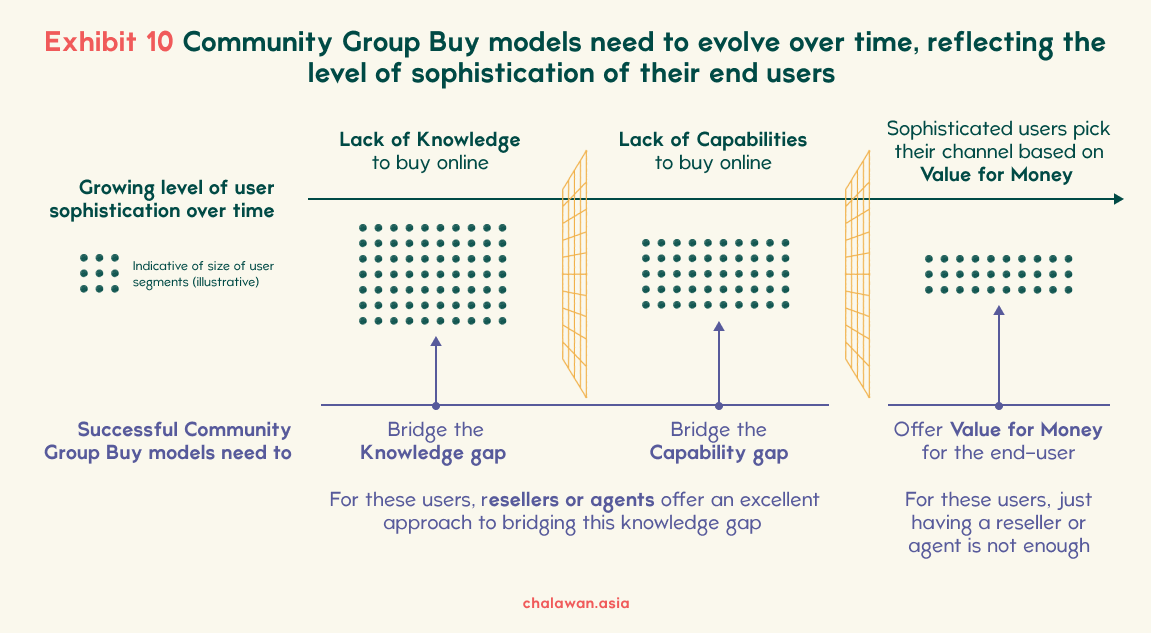

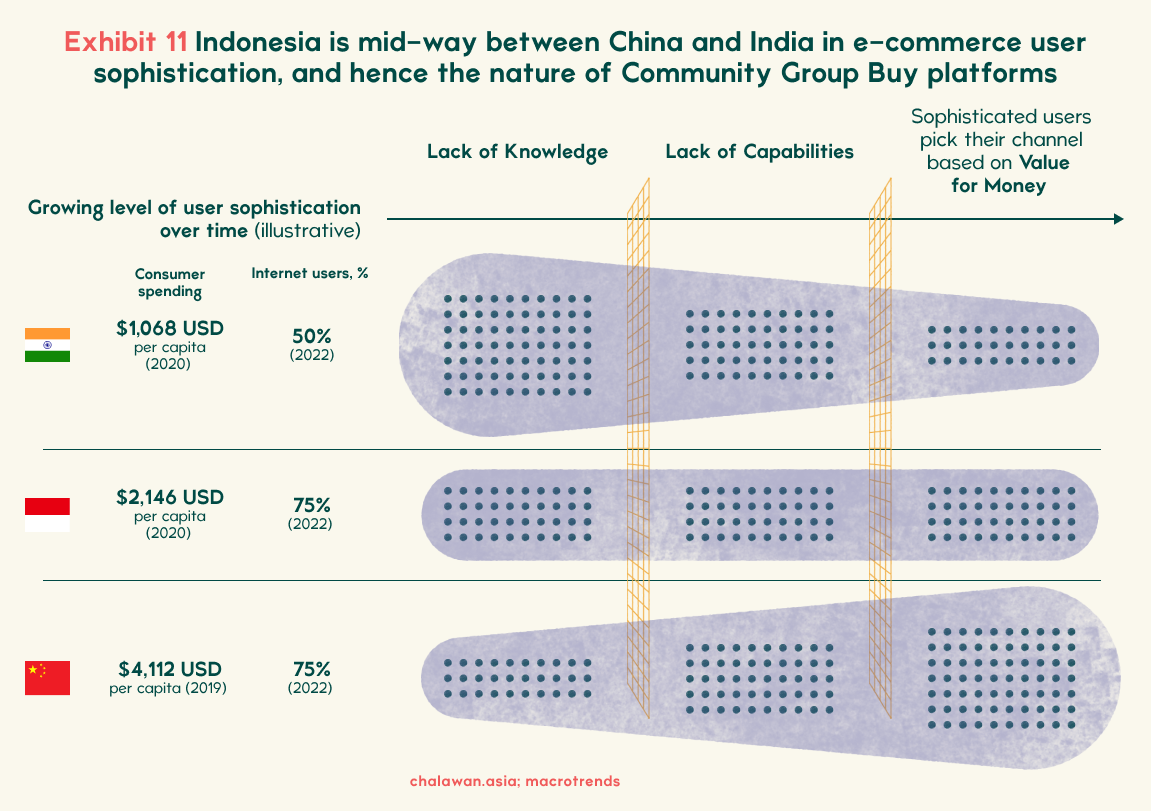

While the e-commerce adoption and usage traits of individual countries differs depending on their culture and consumer preferences, all markets go through the same high-level journey - e-commerce growth is first limited by a lack of knowledge about the channel among consumers, then a lack of capabilities to shop online, and then finally an open search for the best overall value-for-money for a given need or want.

This pathway of growth, and the gradual dissolution of knowledge and capability barriers in favour of open value-for-money competition, is instrumental for assessing the viability and appeal of community group buying in different markets. For example, the agent-led model fares very well in early-stage markets where reseller agents bridge real knowledge and capability gaps in the consuming population, while the price-led model fares better in advanced markets where consumers’ digital literacy and the broader e-commerce infrastructure allow for this more sophisticated way of shopping.

Predicting the prospects of community group buying in Southeast Asia, therefore, hinges on a broader assessment of the digital literacy of the region’s markets versus peers with significant Community group buying activity. We look west to India and north to China:

We have compared India and China with Southeast Asia’s largest market, Indonesia, below:

Based on comparable markers like consumer spending per capita and internet penetration rate, Southeast Asia’s large markets are somewhere in between these two extremes. Indonesia, for instance, lags China in consumer spending per capita, but is already way past India on internet usage. This trend is mirrored across the region, and it allows us to predict the prospects of both community group buy types:

Across both types of Community group buying, a final dynamic worth discussing is the impact of venture capital. In previous posts we’ve detailed the growth and dynamics of Live shopping and Conversational commerce, two social archetypes that have grown from grassroots into wide adoption. Community group buying, on the other hand, has been inserted into the markets much more deliberately by cash-rich platforms that connect sellers, resellers and buyers. They have pitched investors on an ability to disrupt how consumer products are distributed across Southeast Asia, and received generous funding to do so.

Our research indicates that Southeast Asia’s B2C-focused community group buy start-ups have raised more than US$ 500mn over the last four years, and that the closely adjacent set of B2B distribution start-ups have raised more than twice that amount. No matter what else is happening, this shifts the gravitational pull of the model further towards supply-driven rather than raw consumer demand-driven, raising questions about how much of the growth is truly organic.

With the recent chilling of the region’s growth-stage funding climate, and its effect on these start-ups’ ability to raise additional funding, we will all discover the answer to this question soon. Our bet is that 1-3 players will survive in each market, powered by scale and surgical attention to margin optimization across seller payouts, reseller payouts, consumer pricing, and operating costs. The rest will find it hard to keep brands, resellers and end consumers happy at once while starching out enough extra margin to operate profitably.

Whereas social commerce archetypes like Live shopping and Conversational Commerce merely add social traits and value to existing ways of shopping online, Community group buying is a brand-new way to buy and sell consumer goods. It presents a new and different distribution channel for brands, new ways to buy products for consumers, and a new employment option for would-be resellers in the agent-led model.It won’t entirely upend the region’s e-commerce landscape, but will remain an interesting opportunity for emerging cost-conscious brands, or existing ones looking to break into new frontier markets.

For now, we assess the Agent-led community group buying model to apply much better to Southeast Asia than the Price-led model, based on the region’s consumer, infrastructure and digital literacy markers. While a price-led Pinduoduo-like model could emerge in one or several of Southeast Asia’s markets later on, we are not holding our breaths.

The emergence, growth and evolution of community group buying in Southeast Asia has implications for several types of actors: